This proposal of determination of the fair market value of share template has 4 pages and is a MS Word file type listed under our finance & accounting documents.

Sample of our proposal of determination of the fair market value of share template:

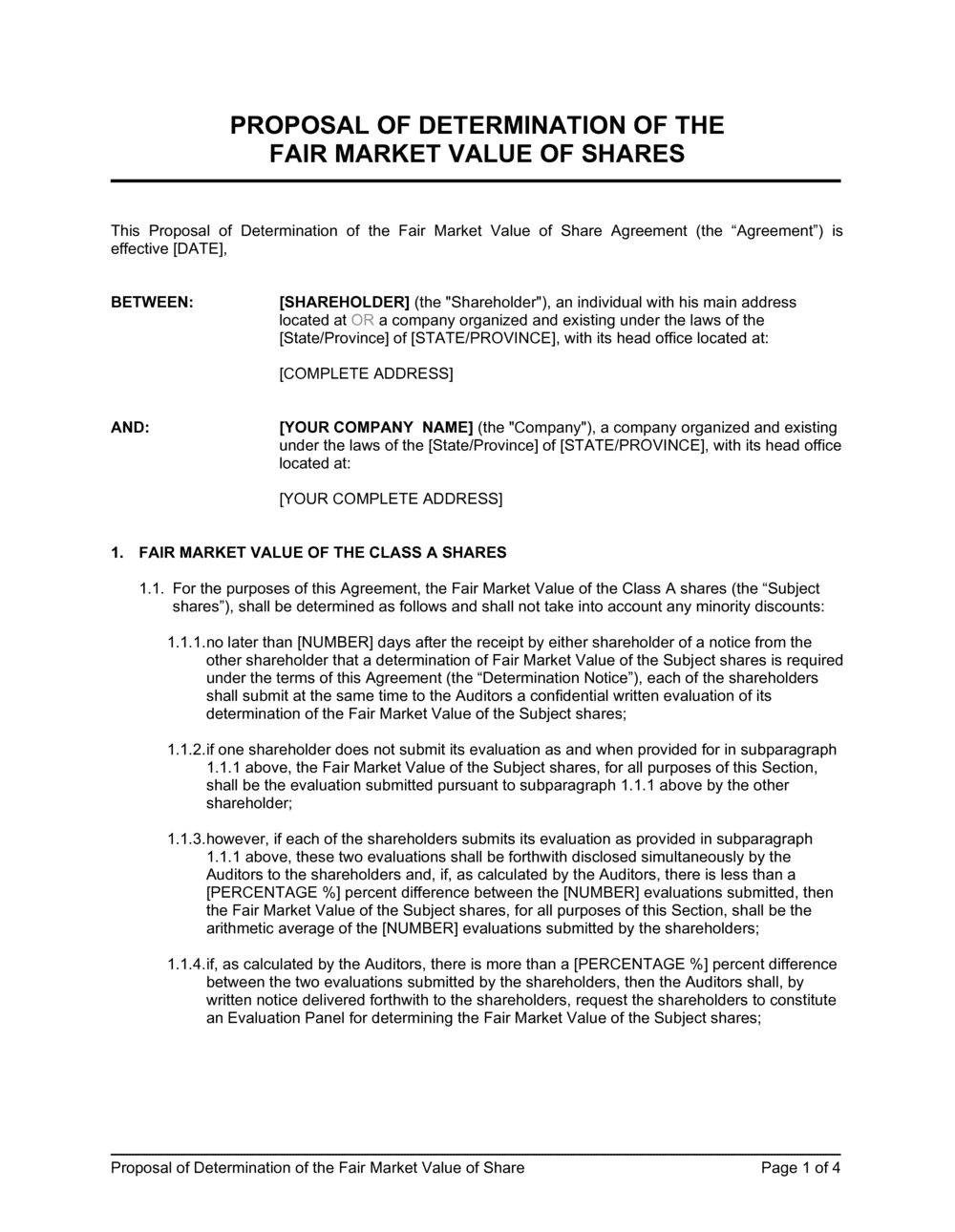

PROPOSAL OF DETERMINATION OF THE FAIR MARKET VALUE OF SHARES This Proposal of Determination of the Fair Market Value of Share Agreement (the "Agreement") is effective [DATE], BETWEEN: [SHAREHOLDER] (the "Shareholder"), an individual with his main address located at OR a company organized and existing under the laws of the [State/Province] of [STATE/PROVINCE], with its head office located at: [COMPLETE ADDRESS] AND: [YOUR COMPANY NAME] (the "Company"), a company organized and existing under the laws of the [State/Province] of [STATE/PROVINCE], with its head office located at: [YOUR COMPLETE ADDRESS] FAIR MARKET VALUE OF THE CLASS A SHARES For the purposes of this Agreement, the Fair Market Value of the Class A shares (the "Subject shares"), shall be determined as follows and shall not take into account any minority discounts: no later than [NUMBER] days after the receipt by either shareholder of a notice from the other shareholder that a determination of Fair Market Value of the Subject shares is required under the terms of this Agreement (the "Determination Notice"), each of the shareholders shall submit at the same time to the Auditors a confidential written evaluation of its determination of the Fair Market Value of the Subject shares; if one shareholder does not submit its evaluation as and when provided for in subparagraph 1.1.1 above, the Fair Market Value of the Subject shares, for all purposes of this Section, shall be the evaluation submitted pursuant to subparagraph 1.1.1 above by the other shareholder; however, if each of the shareholders submits its evaluation as provided in subparagraph 1.1.1 above, these two evaluations shall be forthwith disclosed simultaneously by the Auditors to the shareholders and, if, as calculated by the Auditors, there is less than a [PERCENTAGE %] percent difference between the [NUMBER] evaluations submitted, then the Fair Market Value of the Subject shares, for all purposes of this Section, shall be the arithmetic average of the [NUMBER] evaluations submitted by the shareholders; if, as calculated by the Auditors, there is more than a [PERCENTAGE %] percent difference between the two evaluations submitted by the shareholders, then the Auditors shall, by written notice delivered forthwith to the shareholders, request the shareholders to constitute an Evaluation Panel for determining the Fair Market Value of the Subject shares; Each of the shareholders, by written notice to the Auditors delivered no later than [NUMBER] days after the delivery of the aforementioned notice by the Auditors, shall designate an evaluator (the "Evaluator") which is not an evaluator listed in the most recent list of Third Evaluators; in the event one of the shareholders fails to designate an Evaluator within such than [NUMBER]-day period, the Fair Market Value of the Subject shares, for all purposes of this Section, shall be the evaluation previously submitted by the other shareholder who has so designated an Evaluator; if both shareholders designate an Evaluator within the [NUMBER]-day period, either shareholder may request the party whose name appears first on the then current List of Third Evaluators to act as Third Evaluator on the Evaluation Panel, and, if the first party refuses or is unable to act, then the second and if it refuses or is unable to act, then the third and if it refuses or is unable to act, then the fourth; upon selection of the Third Evaluator, the Evaluator Panel will be constituted on such date comprising the three Evaluators so designated; if, at any time, any Evaluator shall resign, it may be replaced by the party designating it or, if the Third Evaluator resigns, it shall be replaced by the next Third Evaluator on the then current List of Third Evaluators, provided that in no case will the time limits herein set forth be extended to accommodate such replacement; the Evaluation Panel shall, within [NUMBER] days after it is constituted, produce and deliver to the Auditors and to the shareholders, a written submission pertaining to the methods agreed upon by the Evaluators for the purposes of the determination of the Fair Market Value of the Subject shares (the "Methods of Evaluation"); in the event that the Evaluators cannot agree on such Methods of Evaluation, the method determined by the Third Evaluator shall be the written submission for this purpose; notwithstanding any provisions to the contrary, such Methods of Evaluation shall have to set a price for the Fair Market Value of the Subject shares, which price should not take into account the existence of any Special Purchaser as this expression is hereinafter defined in subparagraph 1.1.14;