If you are a business owner that makes your money providing goods or services to other businesses, you’ll most likely want to reward your good customers and make order-placing easier on them by extending credit. Let’s face it; businesses tend to spend more when they have a line of credit open to them. So it only makes sense that you can expand your business and increase your sales by providing a credit plan to your customers. This will allow them to purchase products or services today and pay for them at a later date. In order to accomplish this, you’ll want to add a credit application form to your toolbox of business templates. We have a few for you to download on this page.

If you’re a business that does work with consumers, extending credit is still an option for you. The risk that comes with extending credit directly to consumers is much greater, so you’ll need to use a credit application form and credit check to make a decision. Small retailers make up for this risk by charging higher interest rates. If your customers mostly make small purchases, it may not be a good idea to extend any credit. However, if you’re a private caterer who helps affluent people plan their parties, you may find that extending credit can help you grow your business. A credit application form will help secure the credit you extend by making sure that your customers have a stable track record of honoring their debts.

Why Should I Extend Credit Using a Credit Application Form?

Not sure you’re ready to extend credit? Think of it this way; you’re probably already doing it. Every time your business accepts credit card payments, checks, or even sends invoices to customers, you’re essentially extending credit. You accept these payment types on the assumption that customers will have the funds to pay for the transaction. The only difference is that when you’re accepting credit card payments, your merchant account provider shoulders the risk. However, when you extend credit through invoices or checks, the risk is transferred to you. You’re responsible for verifying and accepting payments and managing the risks that come with them.

Business Credit Application by Business in a Box

Some industries, such as construction companies or manufacturers, often extend credit by invoicing. Invoices are typically due net 30 days or 30 days from receipt.

One of the main reasons businesses offer credit is to help customers focus less on prices and more on their needs. Having a credit option can help you make more sales and enhance your relationship with your customer.

It’s important to note that extending credit will cost you money if it’s done incorrectly. When you sell something on credit, you won’t have immediate reimbursement and you will need to temporarily make up for the cost, which usually means borrowing cash flow from other areas of your operating capital.

And if something happens and your customers are unable to pay, you may end up spending money on collection activities and other costly measures to try to recoup your losses.

Before handing out a credit form to all of your big customers, make sure that you have a legitimate business reason to extend credit. Assess the risks of having several of your larger customers default. If a financial crisis occurs, will you be able to stay afloat without counting your outstanding invoices as income? If you can’t shoulder much risk, it may not be the right time to extend credit to your customers. You should be able to extend credit without becoming overly reliant on it for income. In other words, your cash flow is your cash flow, and outstanding invoices may or may not be paid. Will it hurt your cash flow to extend credit that may not be paid back? If so, it may not be the right time to offer credit options to your customer base.

Do you need a Credit Application? Download it Here

Establishing A Credit Application Process

Long before you offer credit to your customers, you’ll need to decide how you will manage credit accounts. You’ll need to know if you can charge late fees (and how much you can charge) as well as collection laws in your area.

At this point, you’ll want to speak with a lawyer to understand the policies and procedures that are in place in your state when it comes to extending credit. Consumer protection laws vary widely, and there’s a lot of room for error. To abide by these laws, you’ll want to create a uniform process for extending credit and clearly map out your policies. Here are a few things to think about:

- Who are your ideal customers? Will you offer credit to individuals or businesses?

- What company will you use to run credit checks for your customers when they apply for credit?

- What are your payment policies? When will bills be due? What payment options will you offer?

- Who will your customers with credit plans contact when they have a question?

- How will you invoice your customers?

- Will you outsource any of these tasks to another company?

- Have you developed a privacy policy for protecting consumer information?

- How will you keep sensitive financial data safe?

- What’s our game plan for collecting late or delinquent account payments?

- What other considerations do you need to assess to comply with local laws?

Using these questions, you can create a firm credit policy that outlines everything from interest rates to procedures when a customer faults. Your customers should get a copy of these items in the mail once a year and be notified of changes. Usually, this is called “Terms and Conditions” and they can change according to the local as well as federal laws. Your terms and conditions should contain all legal information, dispute resolution procedures, and information on what happens when you must place an account in collections.

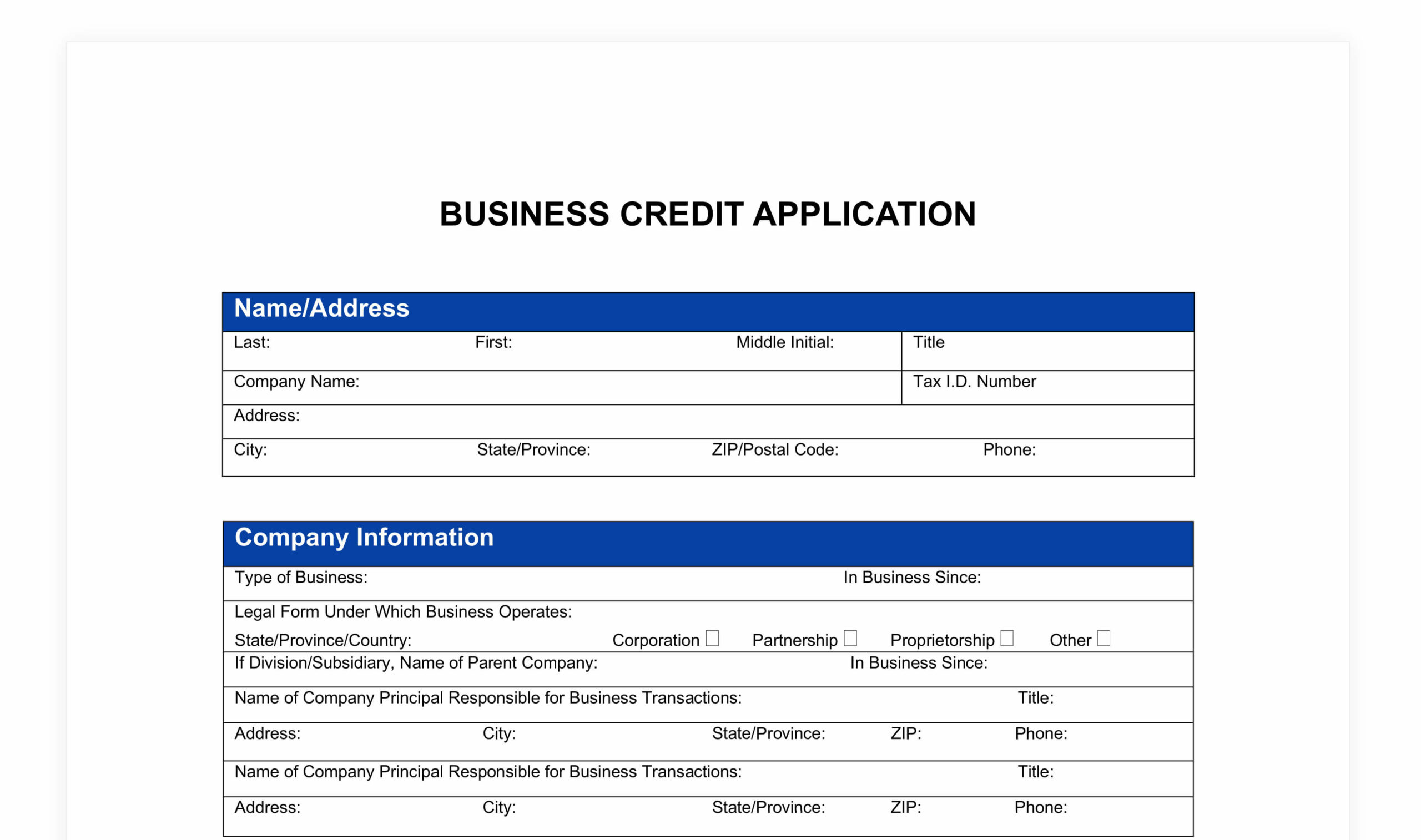

What Should My Credit Application Template Include?

When you’re preparing to launch a new credit program for your customers, you’ll need to get and keep all of your customers’ details in writing and regularly ask them if the information is correct when you send the statement in the mail. The application you use will have important documentation in case of fraudulent or delinquent credit transactions.

Other information that you will need on your credit application template:

- Income verification: For individuals, this means that you’ll want tax documents, bank statements, or the number of the HR department to confirm details of employment. For businesses, you may ask for a profit and loss statement, bank statements, tax documents, or other information that shows their regular profit.

- References: You will need to ask for financial references. For consumers applying for credit, this means banks, credit accounts, etc. For businesses applying for credit, this means vendors and any other creditors that they may have.

- Addresses: Addresses that an individual has lived at in the past two years are an important part of pulling a credit report. You’ll want to know what states, counties, and towns the individual has lived in so you can pull an accurate credit report. For a business, you’ll want all of the addresses the company does business at.

- Contact Phone Numbers: For individuals, this will be their cell phone, home phone, and work phone number. For businesses, you’ll want to get information on who is responsible for paying invoices.

- Tax ID and other identifying information: For individuals, this is their social security number. For businesses, you’ll want their tax ID and employer ID.

- Background information, assets: For individuals, you’ll want the names of their last two employers, employment dates, and any collateral such as equity in a home. For employers, you’ll want to know what type of equity they can offer, and how long they’ve been in business, and may even request backup documents such as a copy of the business plan.

- Signature: This is absolutely essential. Do not process a credit application without a signature giving permission for you to pull a credit report.

- Personal Guarantees: Some individuals will have somebody with a better credit record co-sign their credit application forms. That’s fine, but you’ll want to get all the information for this individual, as well, preferably on another application form. If you’re extending credit to a business, you’ll want to get personal details from the individual responsible for payment if the business fails to pay on time. This will usually be an officer of a corporation, the CEO, or another person in an upper management position.

Source: templatelab.com